Dublin, Jan. 23, 2024 (GLOBE NEWSWIRE) — The “AI and Semiconductors – A Server GPU Market – A Global and Regional Analysis: Focus on Application, Product, and Region – Analysis and Forecast, 2023-2028” report has been added to ResearchAndMarkets.com’s offering.

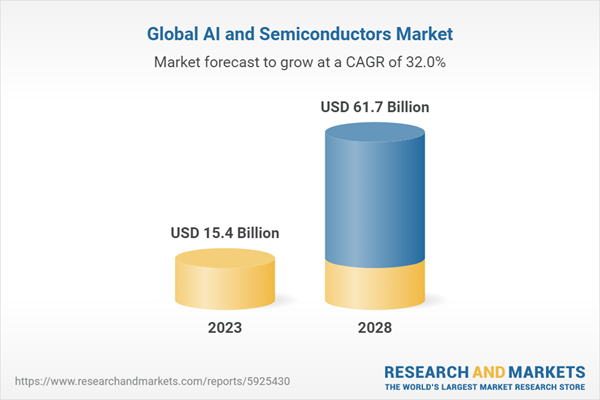

The global AI and semiconductor – a server GPU market accounted for $15.4 billion in 2023 and is expected to grow at a CAGR of 31.99% and reach $61.7 billion by 2028. The proliferation of edge computing, where data processing occurs closer to the source of data generation rather than relying solely on centralized cloud servers, is driving the demand for GPU servers. The increasing trend toward virtualization in data centers and enterprise environments is also a significant driver for GPU servers.

The rapid development of machine learning and artificial intelligence applications is a major driver of this trend. A key element of AI and ML is the training of sophisticated neural networks, which is accelerated in large part by GPU servers. Companies such as Nvidia, for instance, have noticed a spike in demand for their GPU products, such as the Nvidia A100 Tensor Core GPU, which is intended especially for AI tasks. The global AI and semiconductor – server GPU market is growing as a result of the use of GPU servers by a variety of industries, including healthcare, finance, and autonomous cars, to handle large datasets and increase the precision of AI models.

The end-use application segment is a part of the application segment for the worldwide AI and semiconductor – server GPU market. Cloud computing (private, public, and hybrid clouds) and HPC applications (scientific research, machine learning, artificial intelligence, and other applications) are included in the end-use application sector. The global AI and Semiconductor – a server GPU market has also been divided into segments based on the kind of facility, which includes blockchain mining facilities, HPC clusters, and data centers (including hyperscale, colocation, enterprise, modular, and edge data centers).

According to estimates, the data center category will have the biggest market share in 2022 and will continue to lead the market during the projection period. The push toward GPU-accelerated computing in data centers is fueled by GPU technological breakthroughs that provide increased energy efficiency and performance. GPU servers can transfer certain computations from conventional CPUs to GPU servers, which improves overall performance and reduces energy consumption. Consequently, the increasing use of GPU servers in data centers is in line with the changing requirements of companies and institutions that want to manage the sustainability and efficiency of their data center operations while achieving higher levels of processing capacity.

The push toward GPU-accelerated computing in data centers is fueled by GPU technological breakthroughs that provide increased energy efficiency and performance. GPUs offer an efficient way to strike a balance between processing capacity and power consumption, which is something that data center operators are looking for in solutions. GPU servers can transfer certain computations from conventional CPUs to GPU servers, which improves overall performance and reduces energy consumption. Consequently, the increasing use of GPU servers in data centers is in line with the changing requirements of companies and institutions that want to manage the sustainability and efficiency of their data center operations while achieving higher levels of processing capacity.

Data center expansion and the rise of cloud computing services have further propelled the demand for GPU servers in North America. Cloud service providers, including industry giants such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, are investing heavily in GPU infrastructure to offer customers high-performance computing capabilities on a scalable and cost-effective basis. This trend is particularly prominent as businesses increasingly rely on cloud-based resources for AI training, simulation, and other GPU-intensive tasks.

Demand – Drivers, Challenges, and Opportunities

Market Drivers:

GPU server producers can capitalize on this need by providing customized cryptocurrency mining solutions, including rigs specifically designed for mining, cloud-based mining services, or GPU-as-a-service platforms. By charging fees, charging subscriptions, or entering into contracts, these systems can make money for the makers while giving miners access to strong and scalable GPU resources.

The need for data center GPUs derives from their key role in AI model training and execution, which is especially advantageous for businesses engaged in computationally demanding tasks like engineering simulations and scientific research. Manufacturers of GPU servers can take advantage of this demand by providing specialized solutions for high-performance computing (HPC) applications, such as GPU-as-a-service platforms, cloud-based GPU services, and dedicated GPU servers. In addition to giving businesses scalable GPU resources, these customized services bring in money for the manufacturers through fees, subscriptions, or contracts.

Market Challenges:

The economies of scale provided by GPU manufacturers, most notably Nvidia, create a significant barrier to entry for manufacturers of data center GPU servers wishing to integrate backward. A company trying to backward integrate into the GPU production process, for example, would find it difficult to achieve equivalent economies of scale. This has an impact on the business’s capacity to maintain overall competitiveness, engage in research and development, and match prices. As a result, it might be difficult for producers of data center GPU servers to achieve comparable economies of scale, which could limit their efficacy in the extremely competitive market. Additionally, a recurring problem for manufacturers of data center GPU servers is the continual innovation by GPU manufacturers, demonstrated by the ongoing development of GPUs, CPUs, and data processing units (DPUs).

Market Opportunities:

OpenAI’s GPT-4, the latest and largest language model, is one specific real-time illustration of how GPU servers may help HPC and AI. It needed a lot of processing power to train on a huge dataset with over 1 trillion words. A significant contribution was made by GPU servers, more especially by Nvidia H100 Tensor Core GPUs, which sped up the training process up to 60 times faster than CPUs alone. Mixed-precision training was used to achieve this acceleration by optimizing both calculation performance and memory use. Because of this, GPT-4 might be trained in a few short weeks and accomplish cutting-edge results in challenges involving natural language processing.

Artificial intelligence (AI) and advanced analytics play a crucial role in smart cities as they optimize resource allocation, enhance public safety, and improve overall quality of life. Due to their suitability for AI and analytics workloads, GPU servers are becoming an essential part of the infrastructure for the development of smart cities.

Market Segmentation:

Segmentation by Application (End User)

- Cloud Computing

- HPC Application

Segmentation by Product (Configuration Type)

- Single GPU

- Dual to Quad GPU

- High-Density GPU

Segmentation by Region

- North America – U.S. and Rest-of-North America

- Europe – Germany, France, Netherlands, Italy, Ireland, U.K., and Rest-of-Europe

- Asia-Pacific – Japan, China, India, Australia, Singapore, and Rest-of-Asia-Pacific

- Rest-of-the-World – Middle East and Africa and Latin America

Some prominent names established in this market are:

GPU Manufacturers

- Nvidia Corporation (Nvidia)

- Advanced Micro Devices, Inc. (AMD)

- Intel Corporation (Intel)

Server GPU Manufacturers

- Dell Inc.

- Penguin Computing, Inc.

- Exxact Corporation

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 127 |

| Forecast Period | 2023 – 2028 |

| Estimated Market Value (USD) in 2023 | $15.4 Billion |

| Forecasted Market Value (USD) by 2028 | $61.7 Billion |

| Compound Annual Growth Rate | 31.9% |

| Regions Covered | Global |

Key Topics Covered:

1 Market

1.1 Industry Outlook

1.1.1 Ongoing Trends

1.1.1.1 Timeline of GPU and Server Design Upgrades

1.1.1.2 Data Center Capacities: Current and Future

1.1.1.3 Data Center Power Consumption Scenario

1.1.1.4 Other Industrial Trends

1.1.1.4.1 HPC Cluster Developments

1.1.1.4.2 Blockchain Initiatives

1.1.1.4.3 Super Computing

1.1.1.4.4 5G and 6G Developments

1.1.1.4.5 Impact of Server/Rack Density

1.1.2 Equipment Upgrades and Process Improvements

1.1.3 Adaptive Cooling Solutions for Evolving Server Capacities

1.1.3.1 Traditional Cooling Techniques

1.1.3.2 Hot and Cold Aisle Containment

1.1.3.3 Free Cooling and Economization

1.1.3.4 Liquid Cooling Systems

1.1.4 Budget and Procurement Model of Data Center End Users

1.1.5 Stakeholder Analysis

1.1.6 Ecosystem/Ongoing Programs

1.2 Business Dynamics

1.2.1 Business Drivers

1.2.1.1 Surging Demand for Cryptocurrency Mining

1.2.1.2 Rising Enterprise Adoption of Data Center GPUs for High-Performance Computing Applications

1.2.2 Business Challenges

1.2.2.1 High Bargaining Power of GPU Manufacturers

1.2.3 Market Strategies and Developments

1.2.4 Business Opportunities

1.2.4.1 Technological Advancement in High-Performing Computing (HPC)

1.2.4.2 Government Support for Smart City Development and Digitalization

1.3 Global Data Center GPU Market

1.3.1 Market Size and Forecast

1.3.1.1 Data Center GPU Market (by Application and Product)

2 Application

2.1 Global AI and Semiconductors – A Server GPU Market (by Application)

2.1.1 Global Server GPU Market (by End-Use Application)

2.1.2 Global Server GPU Market (by Facility Type)

3 Products

3.1 Global AI and Semiconductors – A Server GPU Market (by Product)

3.1.1 Server GPU Market (by Configuration Type)

3.1.2 Server GPU Market (by Form Factor)

3.2 Pricing Analysis

3.3 Patent Analysis

4 Region

4.1 Global AI and Semiconductor – A Server GPU Market (by Region)

5 Markets – Competitive Benchmarking & Company Profiles

5.1 Competitive Benchmarking

5.2 Market Share Analysis

5.2.1 By GPU Manufacturer

5.2.2 By GPU Server Manufacturer

5.3 Company Profiles

- Nvidia Corporation

- Advanced Micro Devices

- Intel

- Qualcomm Technologies

- Imagination Technologies

- ASUSTeK Computer

- INSPUR

- Huawei Technologies

- Super Micro Computer

- GIGA-BYTE Technology

- Penguin Computing

- Advantech

- Fujitsu

- Dell Inc.

- Exxact

For more information about this report visit https://www.researchandmarkets.com/r/386r

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT:

CONTACT: ResearchAndMarkets.com

Laura Wood,Senior Press Manager

press@researchandmarkets.com

For E.S.T Office Hours Call 1-917-300-0470

For U.S./ CAN Toll Free Call 1-800-526-8630

For GMT Office Hours Call +353-1-416-8900

![]()