The embedded finance market in Latin America offers opportunities in e-commerce, super apps, and B2B segments through embedded credit, payments, and regulatory support. Key drivers include financial access gaps, mobile-first behaviors, and partnerships. Despite regulatory hurdles, market adoption is poised to grow.

Dublin, Nov. 25, 2025 (GLOBE NEWSWIRE) — The “Latin America Embedded Finance Market Size & Forecast by Value and Volume Across 100+ KPIs by Business Models, Distribution Models, End-Use Sectors, and Key Verticals (Payments, Lending, Insurance, Banking, Wealth) – Databook Q4 2025 Update” report has been added to ResearchAndMarkets.com’s offering.

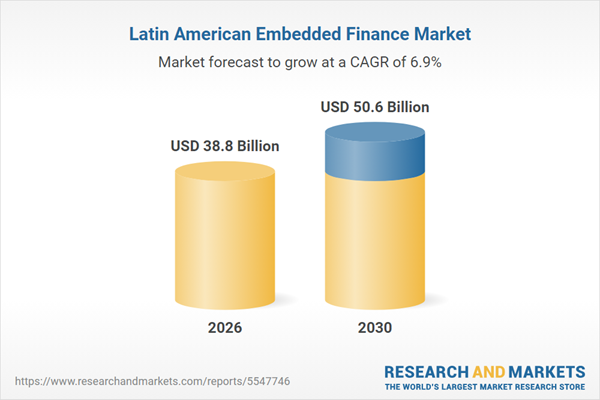

The embedded finance market in Latin America is expected to grow by 9.5% on an annual basis to reach US$38.8 billion by 2025. The embedded finance market in the region has experienced robust growth during 2021-2025, achieving a CAGR of 13.3%. This upward trajectory is expected to continue, with the market forecast to grow at a CAGR of 6.9% from 2026 to 2030. By the end of 2030, the embedded finance market is projected to expand from its 2024 value of US$35.4 billion to approximately US$50.6 billion.

This report provides a detailed data-centric analysis of the embedded finance industry in Latin America, covering five major verticals: payments, lending, insurance, banking, and investments & wealth management. It covers more than 100 KPIs, including transaction value, transaction volume, average transaction size, revenue indicators, and financial performance measures.

The embedded finance competitive landscape in Latin America is marked by platform-led verticalization, deepening partnerships, and growing infrastructure enablers. While Brazil and Mexico lead in terms of ecosystem maturity and competitive intensity, markets like Colombia, Chile, and Argentina are gaining traction through localized innovation and regulatory shifts.

The rise of API-first players, bank-fintech collaborations, and infrastructure consolidation is reshaping how financial products are embedded and distributed. Over the next 2-4 years, the competitive dynamics will continue to evolve – fueled by regulatory enablement, demand from non-financial sectors, and the emergence of cross-border infrastructure providers. However, uneven regulatory progress and localization complexities will remain critical factors shaping entry strategies and competitive positioning across the region.

Platform-Led Models Are Driving Competitive Differentiation Across Verticals

- The embedded finance landscape in Latin America is characterized by vertical integration from large digital platforms that are embedding financial services into their core offerings. E-commerce, delivery, and mobility players are increasingly competing with digital banks and fintechs by owning both distribution and embedded financial products. For example, Mercado Libre operates its own payment infrastructure (Mercado Pago) and credit arm (Mercado Credito), creating a closed-loop embedded finance system that spans payments, credit, and insurance across Brazil, Argentina, and Mexico.

- Major platforms such as Mercado Libre, Rappi, iFood, Nubank, and PicPay are competing both on product breadth and integration depth. These firms are embedding finance into logistics, retail, and lifestyle verticals. Additionally, infrastructure enablers such as Dock, Pomelo, Swap, and Tribal are enabling back-end APIs, regulatory cover, and KYC/AML modules, which allow smaller platforms and merchants to offer financial products without building internal stacks.

- Competitive intensity is expected to remain high over the next 2-4 years, particularly in Brazil and Mexico where infrastructure and demand are more mature. However, gaps still exist in countries like Peru and Ecuador, where fewer full-stack players operate and localized fragmentation persists.

New Entrants Are Targeting Underpenetrated Segments with API-First Strategies

- A new wave of API-first fintech infrastructure providers is entering the Latin American market, targeting niche use cases in credit, compliance, and cross-border payments. Examples include Belvo, which offers open finance APIs across Mexico, Brazil, and Colombia; Klarna’s regional entry through BNPL partnerships; and Swap, which enables white-labeled banking services for startups and marketplaces in Brazil.

- These players are capitalizing on regulatory tailwinds like Brazil’s Open Finance and Mexico’s Fintech Law to provide compliance-ready APIs that reduce time-to-market for embedded finance deployment. Several are offering pre-integrated modules for KYC, fraud detection, and settlement, aiming to lower the entry barrier for non-financial companies.

- New entrants are likely to intensify competition in Tier 2 and Tier 3 geographies and underbanked verticals such as agriculture, transport, and informal commerce. However, fragmentation and localization requirements may slow regional scaling for newer firms without deep local partnerships.

Regulatory Momentum Is Influencing Market Entry and Operational Models

- Regulatory environments across Latin America are evolving in ways that directly impact competition. Brazil has implemented Open Finance protocols that allow for secure financial data sharing, enabling more embedded finance innovation. Mexico’s Fintech Law continues to serve as a blueprint for digital financial services licensing. In 2024, Colombia made progress toward formalizing its Open Finance strategy through the Ruta Regulatoria roadmap.

- These developments create an uneven playing field – markets like Brazil and Mexico offer clearer rules for embedded finance, while countries like Argentina and Peru still operate under fragmented or unclear regulations. The requirement for local licensing or partnerships with regulated entities adds complexity for cross-border players.

- Regulatory alignment across countries is unlikely in the near term. However, Brazil, Mexico, and Colombia are expected to continue leading in licensing innovation, making them the most competitive markets for embedded finance players. Countries with slower regulatory development may see reduced entry by foreign players, reinforcing local dominance.

The Market Is Heading Toward Consolidation and Infrastructure-Led Competition

- As embedded finance scales, infrastructure players are gaining more influence, providing the compliance, orchestration, and operational layers that enable front-end platforms to scale offerings. Firms like Dock (cards and banking-as-a-service), Pomelo (multi-country card issuance and core banking), and Belvo (open banking) are becoming central to the competitive landscape.

- Over the next 2-4 years, consolidation is expected to increase, especially in infrastructure and compliance-heavy segments. Players with regional scale and robust infrastructure capabilities will likely emerge as core enablers, while smaller point-solution providers may either consolidate or focus on niche verticals and geographies.

Embedded Credit Is Scaling Through E-Commerce and Digital Platforms

- Digital platforms are increasingly embedding credit and financing options directly within customer journeys across Latin America, particularly in e-commerce, ride-hailing, and digital marketplaces. Mercado Libre’s credit arm, Mercado Credito, extended over USD 3.3 billion in loans in 2023 alone, mainly targeting small businesses and individual consumers purchasing via its platform. Similarly, Rappi has been embedding BNPL (Buy Now, Pay Later) and credit lines for merchants and consumers through its RappiBank joint venture with Banco Davivienda in Colombia and other countries.

- The expansion of digital commerce, combined with limited traditional credit penetration, is driving the shift toward embedded credit models. Latin America’s large unbanked and underbanked population – estimated at over 200 million by the Inter-American Development Bank – creates a demand for contextual, real-time financing products that can be integrated into transaction flows. Additionally, partnerships between tech firms and local banks (e.g., Nubank and Creditas) are allowing for risk-sharing and regulatory navigation.

- This trend is expected to intensify across Tier 1 and Tier 2 urban centers, as embedded lending models evolve from short-term consumer credit to include SME working capital, equipment financing, and supply chain credit. However, regulatory scrutiny on digital lending practices, especially regarding interest rates and consumer protection, may slow down unregulated BNPL expansion in the region.

Super Apps Are Driving Convergence of Financial and Lifestyle Services

- Latin American super apps are embedding financial services such as wallets, insurance, and micro-investment features within their core ecosystems. Rappi, Nubank, and PicPay have all moved beyond payments to offer a wider range of embedded finance solutions. For instance, PicPay in Brazil has integrated credit cards, insurance, and cryptocurrency investing into its platform, transforming from a payments app to a broad financial ecosystem.

- High mobile penetration, growing consumer comfort with app-based services, and the need to build user loyalty and stickiness have pushed super apps to bundle financial tools. Players are leveraging payments as a gateway to cross-sell more complex financial products. The rising cost of user acquisition in Latin America also incentivizes financial-service layering on existing high-frequency platforms like mobility or food delivery.

- Super app-driven embedded finance is expected to stabilize in Brazil and Colombia, with deeper product integration and cross-border expansion. Newer markets like Peru and Ecuador may see scaled rollouts as mobile-first platforms replicate successful models. The ability to embed services seamlessly while managing regulatory complexity will be key to long-term sustainability.

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 1150 |

| Forecast Period | 2026 – 2030 |

| Estimated Market Value (USD) in 2026 | $13.2 Billion |

| Forecasted Market Value (USD) by 2030 | $18 Billion |

| Compound Annual Growth Rate | 8.1% |

| Regions Covered | Latin America |

For more information about this report visit https://www.researchandmarkets.com/r/83yefg

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com

Laura Wood,Senior Press Manager

press@researchandmarkets.com

For E.S.T Office Hours Call 1-917-300-0470

For U.S./ CAN Toll Free Call 1-800-526-8630

For GMT Office Hours Call +353-1-416-8900

![]()